If you’re interested in dipping your toes into ynab or have tried them out before and haven’t stuck, this guide will explain how to use ynab.

If you’ve been here for a while, you know I love talking about systems that make life easier – meal planning, pantry sorting, and yes… budgeting! One tool that really changed the way I think about money is YNAB (you need a budget). I’ve been using it since 2016 and it’s been a life-changing thing! I’m obsessed with messing around, studying, analyzing and analyzing my budget. I’m always trying to see if there’s a more efficient way.

We also helped coach a small number of people on YNAB budget! It’s not difficult to use the app, but there’s a bit of a learning curve when it comes to wrapping around your brain about how it fits. Getting someone to teach you the hand is the ideal way to learn.

Listen to me on the YNAB Budget NERDS podcast!

Why Ynab works?

Unlike traditional budgets that feel restrictive, YNab is about giving every dollar a job. Instead of guessing what to spend in the future, YNAB works with the money he already has in his account now. It’s also very easy to move money between categories. So if you spend too much food (me every month!), you can cover it with two clicks using your shopping money.

Another surprising thing about it is that you can save on “crunchy” expenses like what you might pay quarterly, or annually, or in rare cases. For example, putting $100 in the Christmas category every month means having the cash you need every Black Friday for holiday shopping. Or the car insurance bill you pay once a year – save a little each month and magically prepare the full amount when your bill is mailed. Your budget will be dialed!

How to use YNAB

Step 1: Sign up and connect your account

Visit the YNAB website to start a free 30-day trial (no credit card required). Then it costs $108 a year. Connect checks, savings and credit card accounts that you use regularly. To keep your budget simple, you tend not to add investments or massive savings. You can explain the money sent to a good place without actually looking at the balance. I mainly focus on check cards and credit cards. Think of your plan as your digital cache envelope system. Connecting all your checking accounts will bring you a ton of money ready for allocation.

Step 2: Allocate money to your credit card

If you have a credit card (which most people do) and you’re going to pay back each month, you’ll want to allocate an amount of dollars that your invoice will likely be in the credit card payment area. So, if you’re ready to allocate $10,000 and currently $2,000 is registered with your credit card, you’re ready to move $2,000 to your credit card and assign the remaining $8,000 to your expenditure and invoice categories.

Step 3: Allocate money to your savings

If you add a savings account to YNAB, you can also move that money to the savings category. The goal here is to leave only the money you need from this month, as you are ready to allocate.

Step 4: Customize the categories (and use emojis!)

Once you have moved your credit cards, savings and other reserved funds aside, you will need a pile of money to allocate them to categories. Before you reach the fun part, check out YNAB’s default categories and customize them to your life!

If you have a pet, please create a pet fee. If you have children, make one for your child. If your mobile phone is being paid through work, remove that category. Think about everything you spend on both the month and year and try creating categories for them. Try to balance good tracking without creating so many people you can’t find anything.

Use emojis in categories to find them more fun and easier on your list!

Finally, group categories in a way that makes sense to you. You can spend monthly and annually. Or + Needs. Or bills, lifestyles, homes, children, etc.

See all my categories in this post: My Budget Categories

Step 5: Consider adding a target

Click on a single category and the target is in the sidebar. The goal of the target is to plan the amount you need for this category each month. As Ben and Ernie said on their recent budget nerd podcast, if you think of YNAB as a digital envelope system, then assigning the category is the money you put in the envelope. The target is the amount you want to start every month.

For example, an automatic recommended gym membership is $500 a month and $97 a month. You don’t need to use targets, but it helps you remember how many invoices each invoice is, or target spending for each category you have decided. It also creates a budget very quickly as all targets can click on Autofill in the future simply by clicking “low funds”!

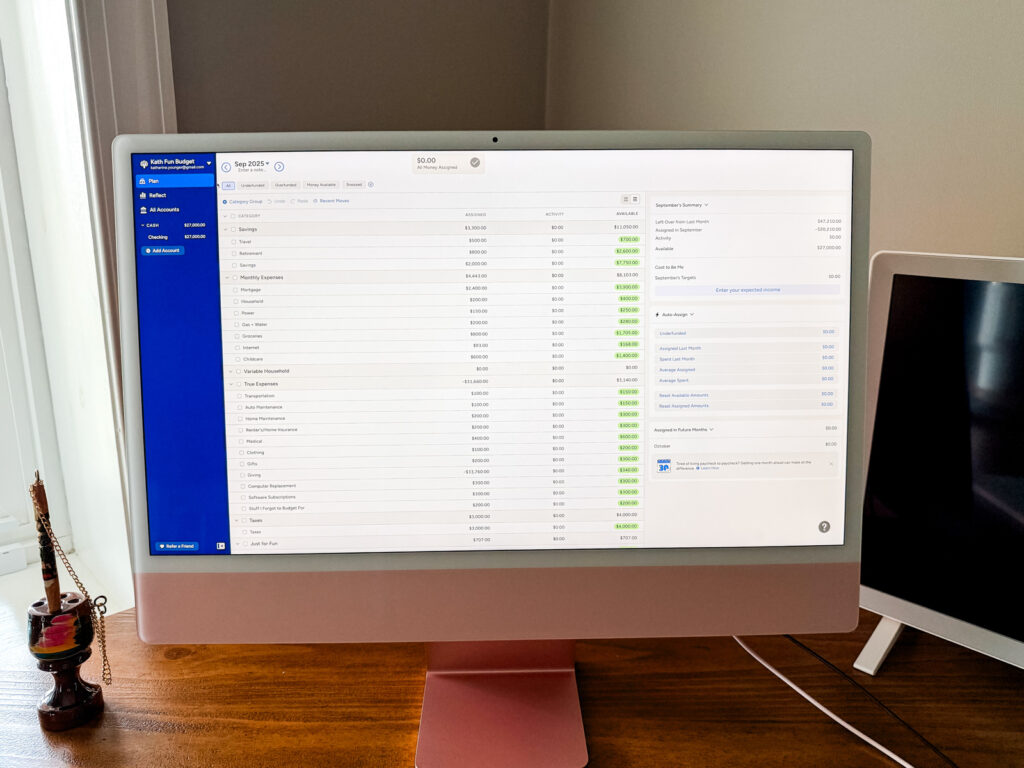

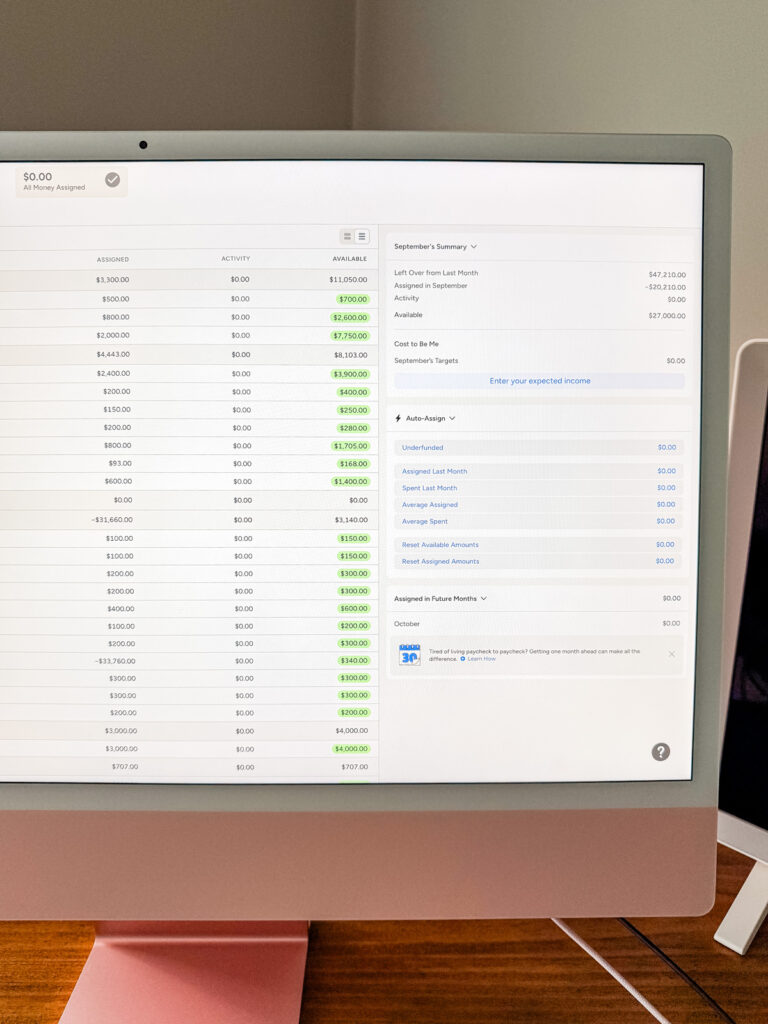

Step 6: Give every dollar a job!

Now is the most fun part! Using a pile of money ready for allocation, start dividing all the dollars you have into your categories. You may need to refer to your check or credit card account to see what you normally spend on things. If you don’t know, just guess from the stadium! You can move money between categories any time if you wish.

Step 7: Fully funded first

Hopefully you’ll get to the end and have a bit more left, but if not, you’ll need to build that buffer so you can fully fund it first. YNAB recommends avoiding your income last month, so you don’t have to worry about the timing of your bill. This also creates a mini emergency fund in a one-month cost buffer in your checking account. As mentioned above, you may need to move some money out of your savings to do this, or you may need to work to save each month a month ahead. This is a big key to stopping your salary from being paid. Ultimately, this will allow you to spend this month with this month’s money. This is when budgeting really started to feel calm and empowered.

Step 8: Don’t forget the savings category

At YNAB, we treat savings like an expense. If you have a repeat 401k transfer, make it look like a cost, and when it debits, it leaves that category. If you’re planning a trip in a year from now, think about how much you think you’ll need and try putting it aside a little each month until you get there.

Step 9: Track your spending as you go

With YNab, you can easily see what remains in each category in real time. you can:

Enter your purchase in the mobile app at checkout. Alternatively, import the bank connection and import the transactions for later classification.

It’s really important to check in your budget as often as possible! Every day is ideal, but don’t wait longer than every week. Otherwise, transactions will be stacked in confusion! It’s very easy to review your app every morning, sort and approve transactions. Make it part of your morning routine. Over time, you start to see patterns, spend more intentionally, and feel less stressed about money.

Try Ynab!

Starting a budget can feel overwhelming, but YNab makes it surprisingly accessible. It’s not like a strict meal, it’s not like a meal plan. It gives structure, freedom, and room for what you love.

Please ask questions in the comments!

Other Ynab posts: